A Blockbuster Week for the Economy

Week in Review: Dec. 11-15

A blockbuster week. Potential game-changer. Benign data on inflation and dovish messaging from the Federal Reserve resulted in surging stock prices and a bond market rally. Jerome Powell said, “A very high proportion of forecasters were expecting very weak growth or a recession. Not only did that not happen, we actually had a very strong year.” That’s true. This year was surprisingly good, and I explain why below. Until you get to that part of our weekly review, let’s start at the most obvious point . . .

Monday

Gas Prices

Gas prices fell for a twelfth consecutive week and are under $3.30/gallon for the first time since late 2022. Gas prices are under $3 in about 20 states.

Diesel Prices

Diesel prices fell below $4.00/gallon for the first time since July.

TSA Checkpoint Travel Numbers

The number of passengers screened by TSA edged back above 2019 levels this past week, but the gap between 2023 and 2019 is far smaller than it was during the weeks leading up to Thanksgiving. Maybe some evidence that consumer spending is starting to slow in travel? Question 1 – consider this and other questions as food for thought.

Tuesday

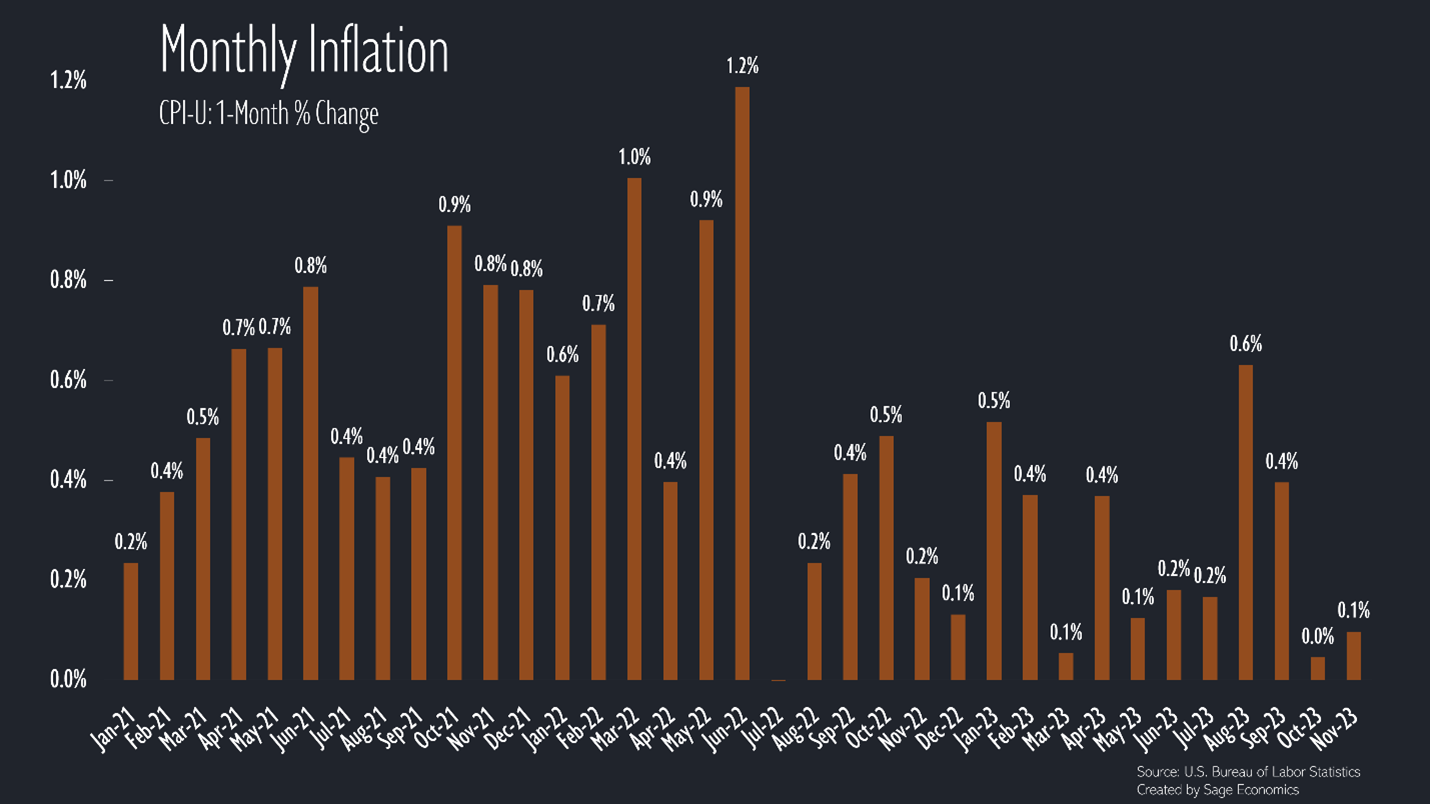

Consumer Price Index (Inflation)

Economywide prices increased just 0.1% in November and are up 3.1% over the past year. Excluding food and energy prices (volatility, geopolitical/noneconomic influences), prices are up 4.0% year over year. That represents the slowest core annual rate of inflation since May 2021. Somehow, those abundant wage pressures have yet to heavily influence the headline numbers. Can that continue? Question 2