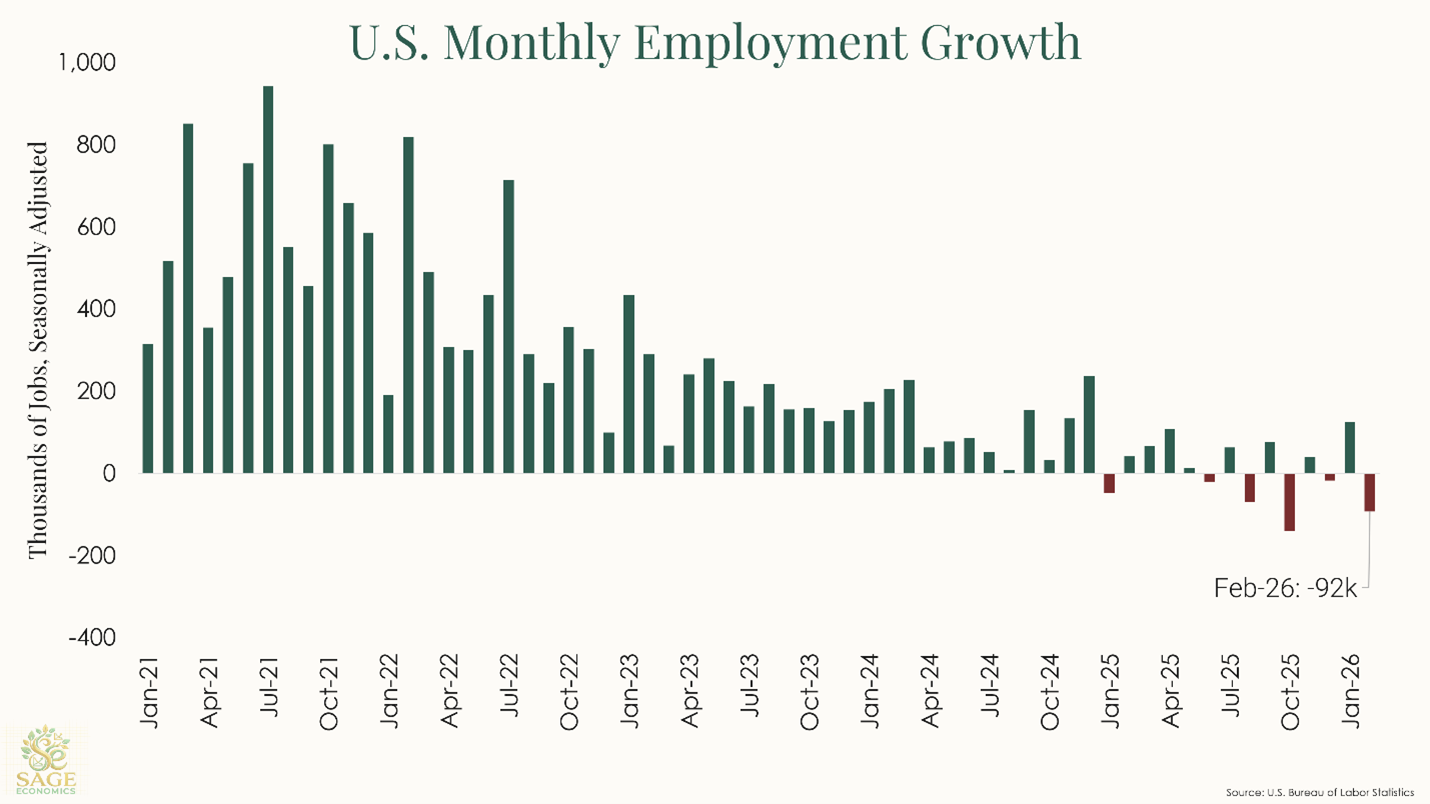

A Brutal Jobs Report

Employment down 92,000 in February

This post is sponsored by KODIAK – Proven Workforce Solutions. I wouldn’t accept a sponsor for this newsletter unless they were 1) a company I trust and 2) addressing critical issues like skilled labor shortages in construction. KODIAK, which recently merged with Pivot, checks both those boxes. Their mission is to help construction companies find experienced talent, including engineers and project managers for Direct Hire, as well as skilled craft professionals like welders and electricians for contingent staffing. With over three decades of experience, I encourage contractors struggling to find workers to consider KODIAK.

Today’s jobs report was, in a word, brutal. U.S. employment fell by 92,000 jobs in February, and December and January’s employment growth was revised down by a combined 69,000 jobs. The unemployment rate rose to 4.4%.

Employers have added just 156,000 jobs over the past year, and it’s difficult to explain just how atrocious that is. For context, we averaged more than 156,000 per month in every year from 2011 to 2019. As all know, these numbers are subject to revision, so that 156,000 figure could be completely revised away, or worse.

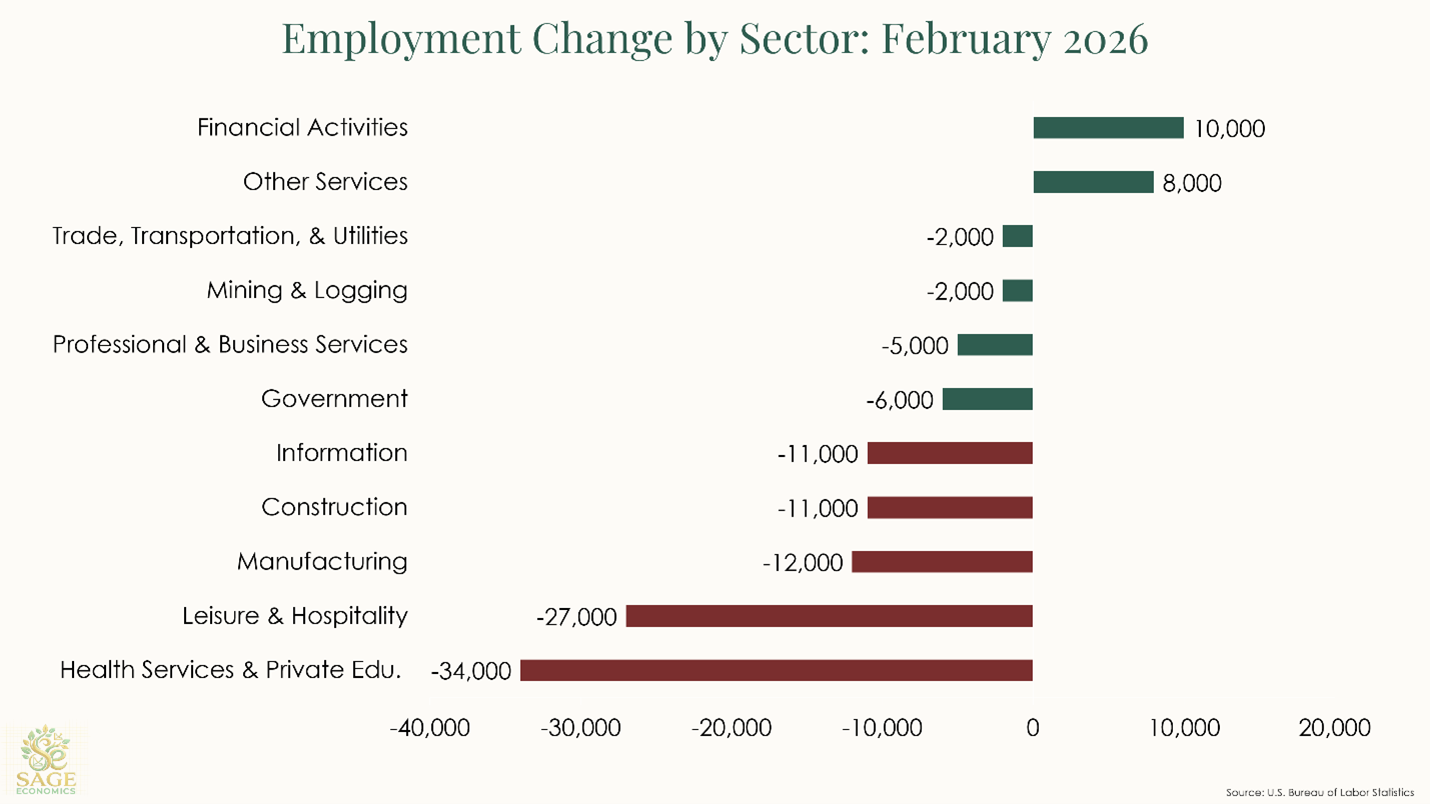

Are there a few caveats to today’s data? Absolutely. A Kaiser strike caused employment to fall in the healthcare segment, and those jobs will presumably come back in March.

The weather was also worse than normal for the month, and that can hurt leisure and hospitality hiring. True, the so-called reference week (when underlying surveys transpire) occurred well before the February 23-24 storms. Nonetheless, there was likely at least some weather impact here based on the poor performance of weather-centric segments like construction and leisure/hospitality.

There was also some shift in methodology that I won’t get into here, but that triggers some additional uncertainty regarding how one should interpret the initial estimate for February jobs.

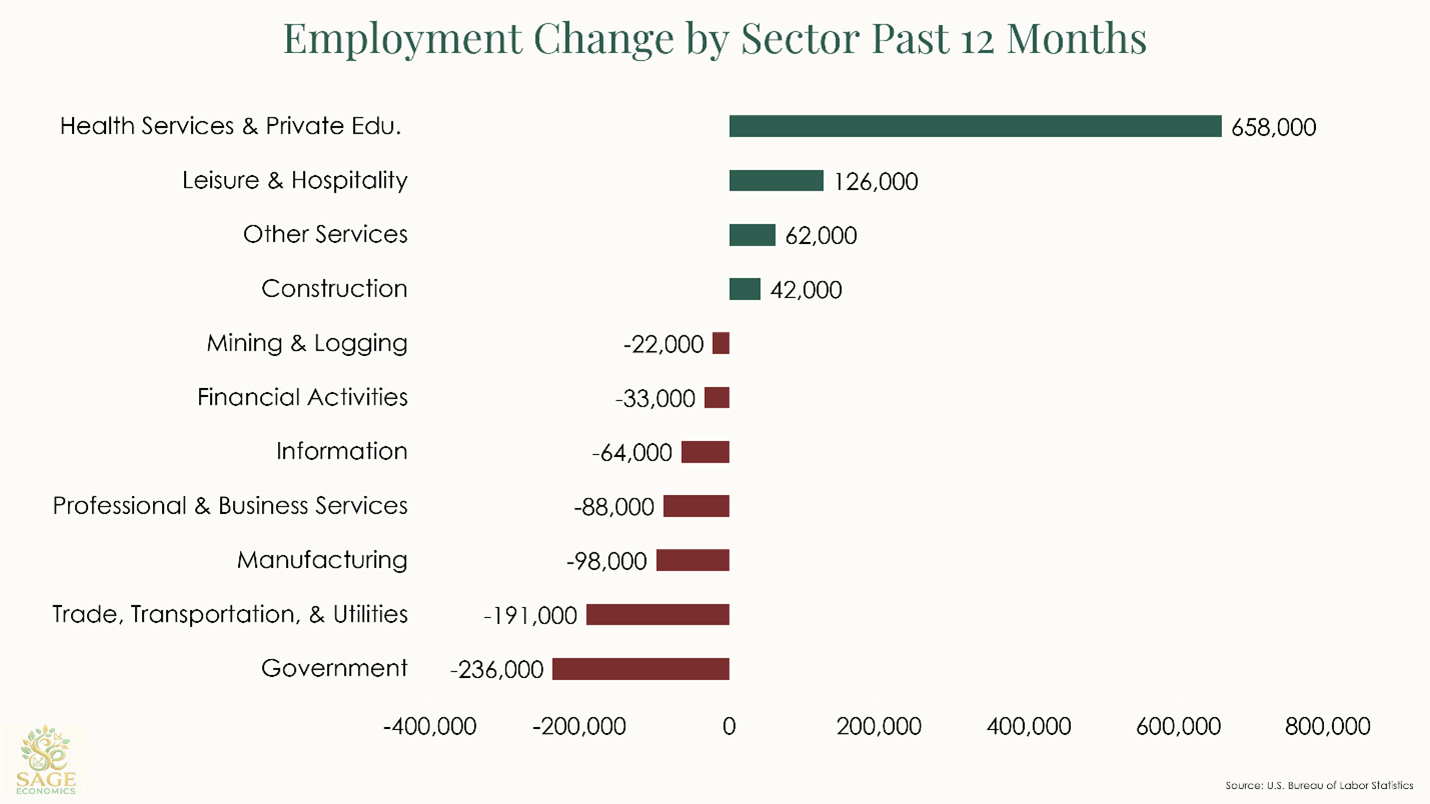

But those caveats don’t change the fact that the labor market is utterly stagnant. What’s (or who’s) to blame? There’s a lot going on, but it’s no coincidence that employment is now lower than it was in April 2025, the month that kicked off our ongoing tariff misadventure. We’ve also observed weaker job growth in industries that typically depend on unauthorized immigrants, although that may be due to cyclical factors rather than immigration policy.

Are there any silver linings in today’s report? Yes, as long as you really squint. The prime age (25-54) employment-to-population ratio ticked down but remains very elevated by recent standards. This economy is fine for anyone who has a job but rather brutal for those in search of one.

The Upshot (Is it Time to Panic?)

Viewed in isolation, no, it’s not time to panic. It’s one bad jobs report, and as mentioned above, there are caveats. But the risk of recession is rising and the economy is becoming increasingly dependent on the AI infrastructure spending boom to drive growth. With oil prices spiking and market values declining, the trajectory is not good. This war needs to end soon, or it could utterly upend the 2026 economy.

What’s Next

This week was loaded with important data releases (beyond just this one), and we’ll cover all of them in Week in Review, our every-Friday post that gives you everything you need to know about the economy in a breezy, five-minute read. That’s just for paying subscribers. If that’s not you and you want it to be, just click the button below: