A Great May Jobs Report

Can good news be bad news?

This post is sponsored by KODIAK – Proven Workforce Solutions. I wouldn’t accept a sponsor for this newsletter unless they were 1) a company I trust and 2) addressing critical issues like skilled labor shortages in construction. KODIAK, which recently merged with Pivot, checks both those boxes. Their mission is to help construction companies find experienced talent, including engineers and project managers for Direct Hire, as well as skilled craft professionals like welders and electricians for contingent staffing. With over three decades of experience, I encourage contractors struggling to find workers to consider KODIAK.

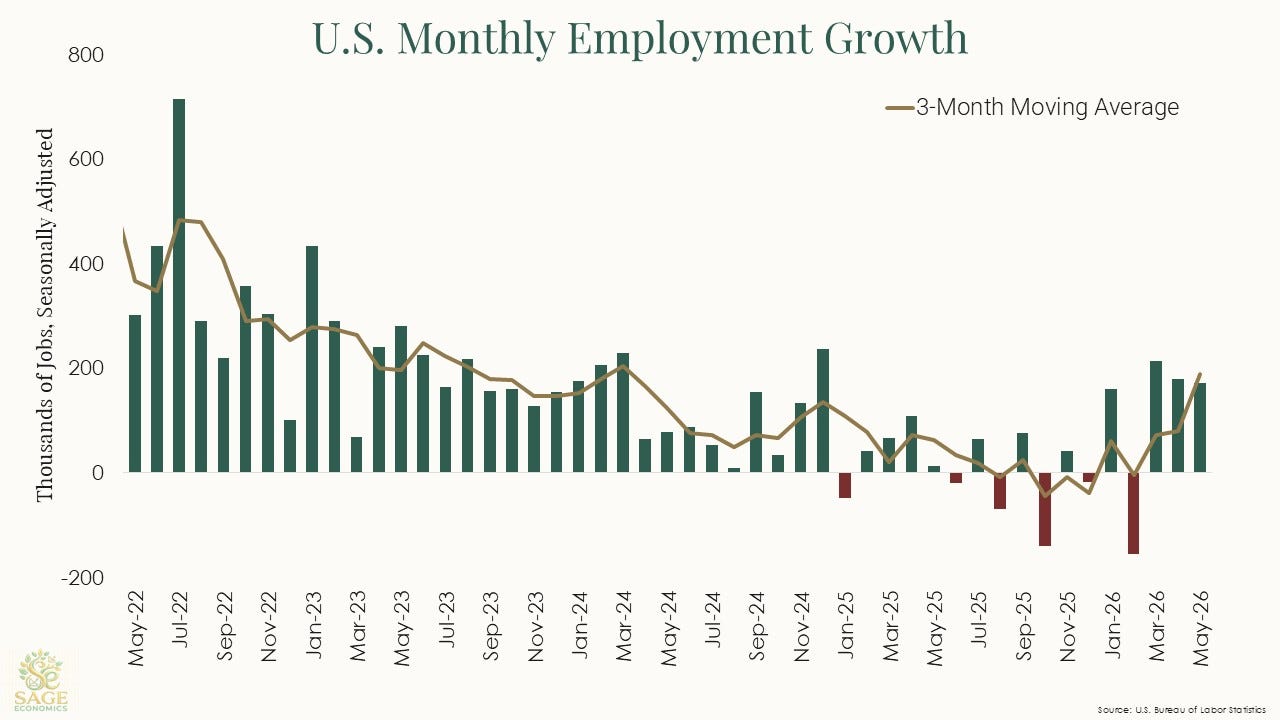

U.S. employers added an impressive 172,000 jobs in May, and March and April’s estimates were revised up by a combined 93,000 jobs. This tramples expectations and suggests the wobbles of 2025 and early 2026 are now decidedly behind us.

There’s not much to dislike here. The unemployment rate stayed at a perfectly acceptable 4.3% (it actually fell slightly when you take it to the hundredths). Prime age (25-54) labor force participation inched up and is close to a cyclical high. Young adult unemployment improved slightly, and fewer people are working part-time for economic reasons.

If you really want to nitpick, long-term unemployment (at least 27 weeks) inched up and is at a cyclical peak, but it’s not particularly high by historical levels, about the same as it was in 2017.

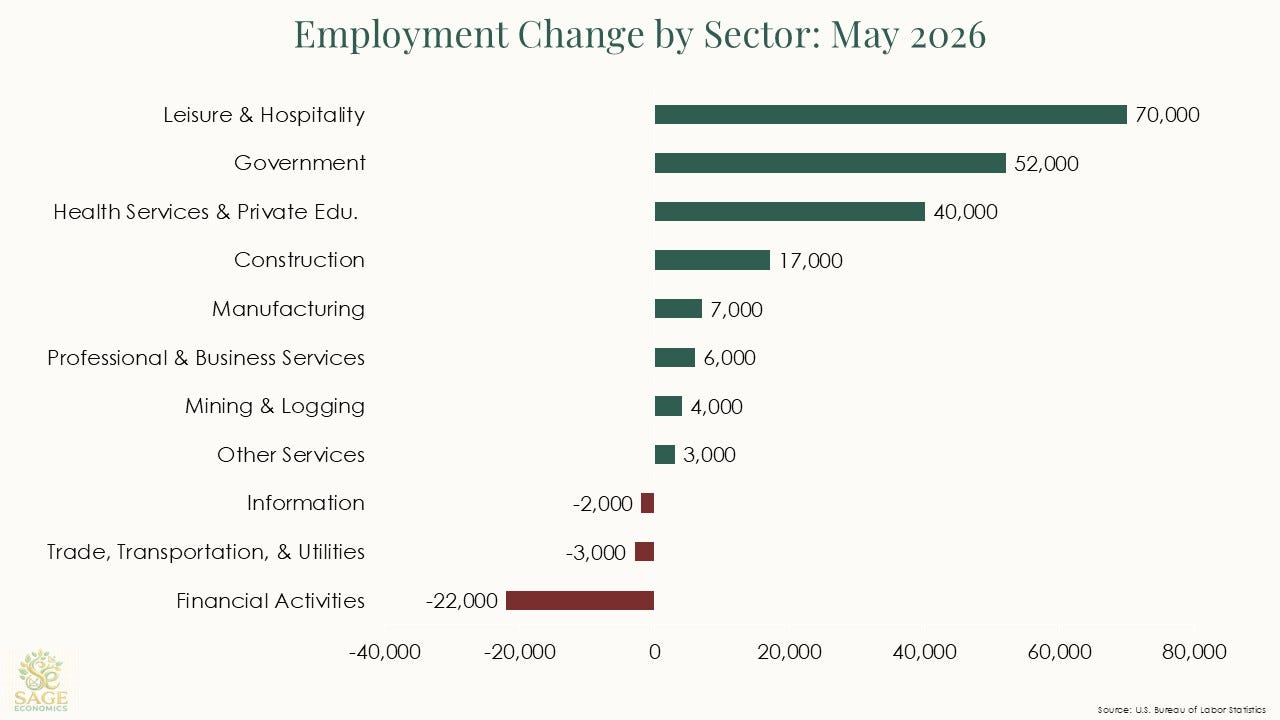

And really, there’s no need to nitpick. Job gains were broad-based by recent standards, though healthcare and leisure and hospitality still dominated growth.

Government also added a surprising 52,000 jobs for the month, the majority of which were noneducational local government positions.

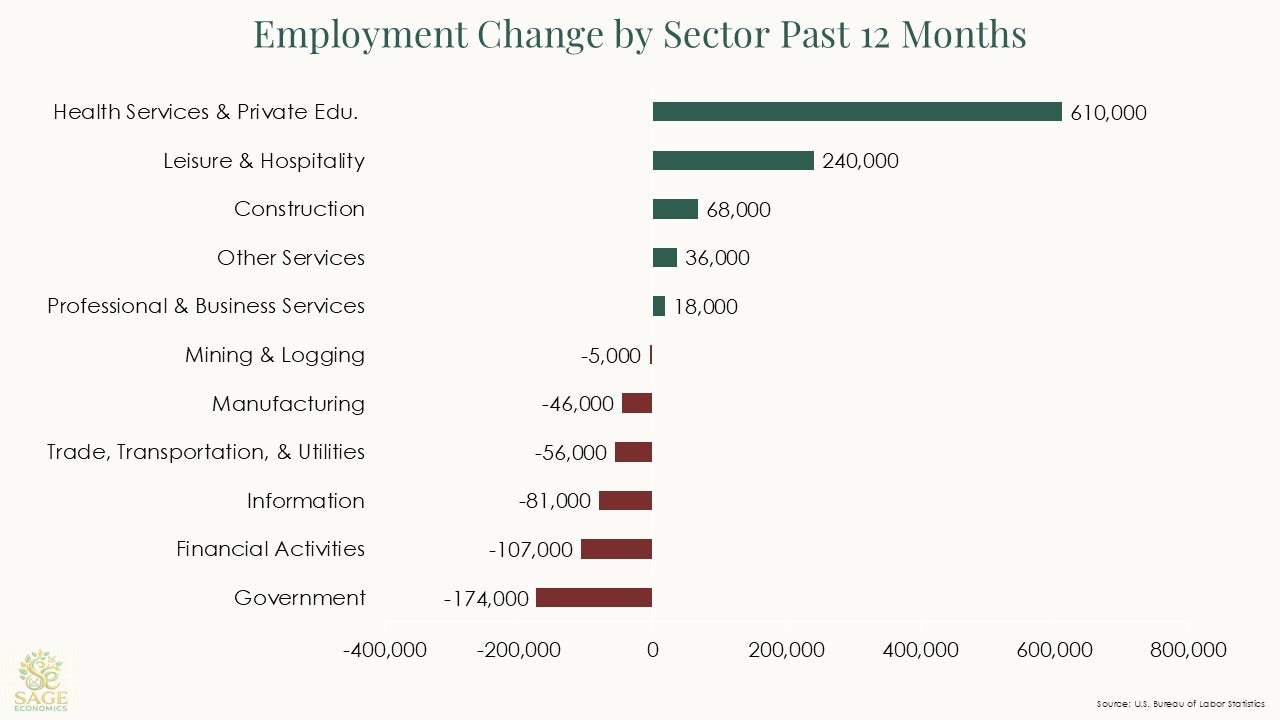

The financial activities sector lost another 22,000 jobs for the month, and employment in that category is now down by more than 100,000 over the past year. While these losses are spread across subsectors, insurance carriers have been hit particularly hard, shedding about 73,000 jobs since May 2025.

For the labor market and broader economic resilience, today’s report is purely good news. And for anyone working in an interest rate segment, today’s report is…I don’t want to say “bad,” but decidedly less good.

Rate Hikes Are (Probably) Coming

The Fed has two jobs: maximize employment and keep inflation at a 2% annual rate. Today’s blowout report suggests the employment side of the mandate is in good shape, while recent inflation data shows price increases are speeding up.

As a result the Fed is now more likely to raise rates then cut them, and those hikes could come sooner than previously expected.

What’s Next

This week was packed with data releases, and we’ll cover all of them in Week in Review, our every-Friday post that gives you everything you need to know about the economy in a breezy, five-minute read.

That will be out in the next few hours and is just for paying subscribers. If that’s not you and you want it to be, just click the button below:

BS🫠🤥

All good and dandy but what about BLS data that is showing that 90% of all new added jobs were foreign born workers?