Another Monster Jobs Report

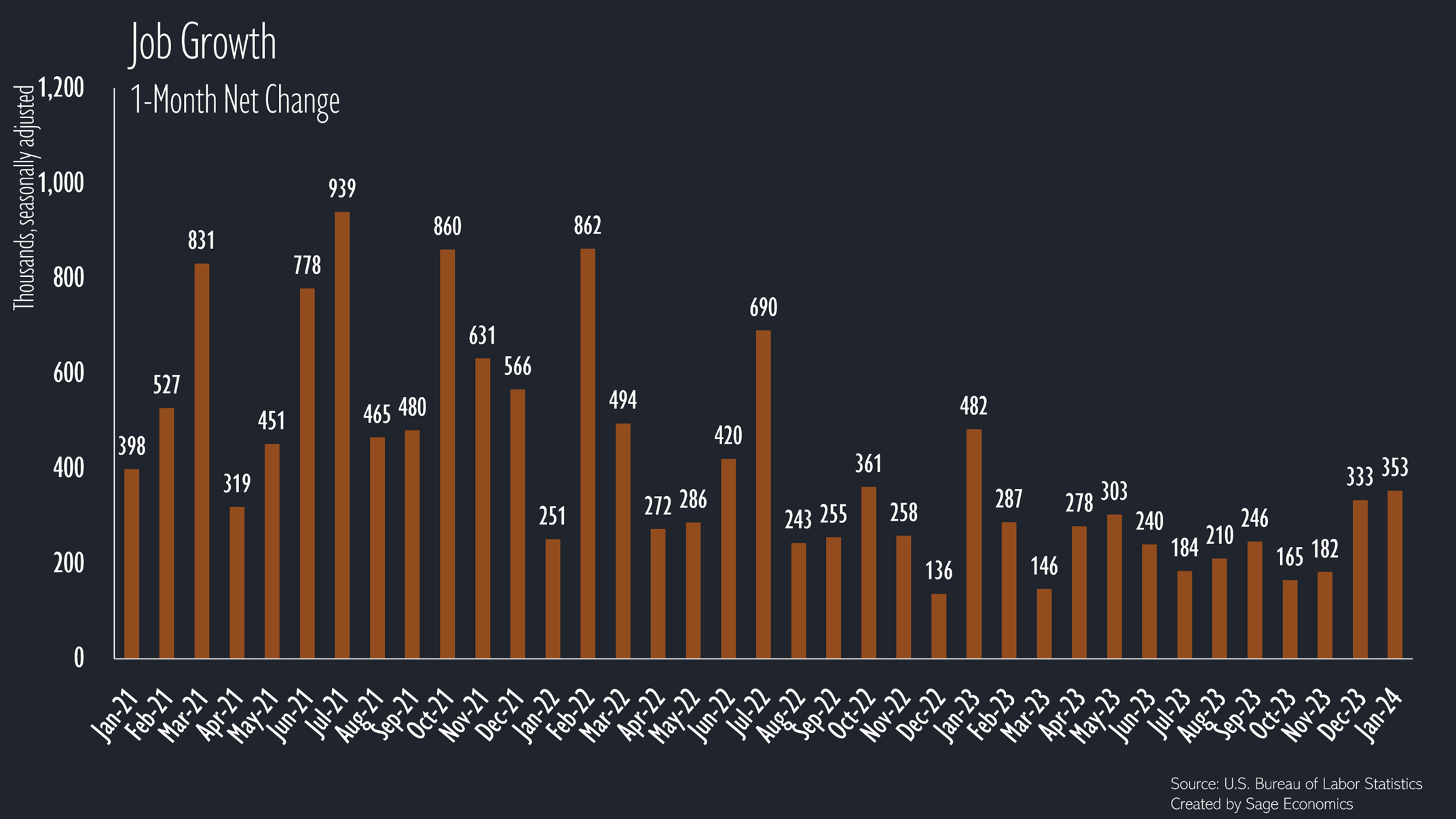

U.S. Employers add 353,000 jobs in January

This post is sponsored by Pivot Workforce. I wouldn’t accept a sponsor for this newsletter unless they were 1) a company I know and trust and 2) tackling an important problem like the construction industry's skilled labor shortages. Pivot checks both those boxes. Their goal is to help construction companies get the high-quality talent they need, and they have over three decades of experience staffing difficult-to-fill positions for some of the most recognized names in the construction industry. I urge any contractors struggling to find workers to give Pivot a look.

The U.S. economy will slow at some point. Maybe a crisis in the banking sector will slam the brakes on growth during the first half of 2024. Maybe an unnoticed asset bubble will pop in 2025. At the very latest, the universe will collapse in 22 billion years, give or take, at which point those predicting a recession will be correct.

That point definitively did not come in January 2024, when U.S. employers added an incredible 353,000 jobs. That’s about twice as many jobs as they were expected to add, and revisions to November and January’s job growth tacked on another 126,000. Over the past three months, employers have added 868,000 jobs, the most in any three month period since the first quarter of 2023.

Meanwhile, the unemployment rate was unchanged at 3.7%, just spitting distance above the lowest level in half a century.

How does the economy keep surprising to the upside? It’s got something to do with a slew of highly visible layoff announcements that have virtually no impact on the overall labor market.

You might have seen that the Wall Street Journal, Time Magazine, Business Insider, The L.A. Times, Pitchfork, and the Messenger all announced layoffs over the past month. That seems bad, sure, but collectively amounted to fewer than 900 total positions lost, or roughly 0.0006% of all jobs in the U.S.

Industry Level Data

Job gains were, once again, concentrated in education and health services, with most of those jobs coming in the healthcare sector. Trade, transportation, and utilities added jobs at the fastest rate since February as both the retail and trucking sector continue to recover from a rough 2023.

The only sector that lost jobs was mining and logging, and that’s got a lot to do with frigid temperatures stalling extraction work.

Odds and Ends

The share of employed people with multiple jobs fell to 5.1% in January. That’s the exact same rate as in February 2020. Perhaps counterintuitively, this measure is down significantly since the mid-1990s.

Temporary help services (think staffing firms) added jobs for the first time since March 2022. This is typically thought to be a sign of job growth (or losses) a few months down the road, meaning those looking for doom and gloom lost yet another talking point (albeit a small one).

Just 56% of Current Employment Statistics Surveys were filled out in January. While that’s up from 49% in December, it’s the lowest rate for a January since 2002. While this seems really low, revisions are based on surveys that come in late, and the response rate typically rises to at least the high 80% range by the time the final employment estimate is released.

What’s Next

Anirban is currently working on Week in Review, which will go out to paying subscribers later today. If that’s not you and you want it to be, just click the link below.

Zack-- all those economists/media outlets that kept saying the economic sky was going to fall for soooooo long-- how much blame would you assign to them for the public being soooo negative about the economy? Yeah, yeah, I know people are getting a bit more optimistic (how can they not with so much factual evidence in front of them) but most people were more pessimistic about the economy than they were during the 2008 crash.