Are delinquency rates rising?

Checking in on borrowers

In 2014, Rihanna recorded a song called “Bitch Better Have My Money.” It probably resonated with a lot of commercial banks; the delinquency rate on all loan types was over 3% at the time.

As of Q1 2023, that rate stood at 1.2%, behind only Q4 2022 for the lowest on record (and the record goes back to 1987). Which is to say, despite inflation and a few other economic headwinds, bitches are still getting banks their money.

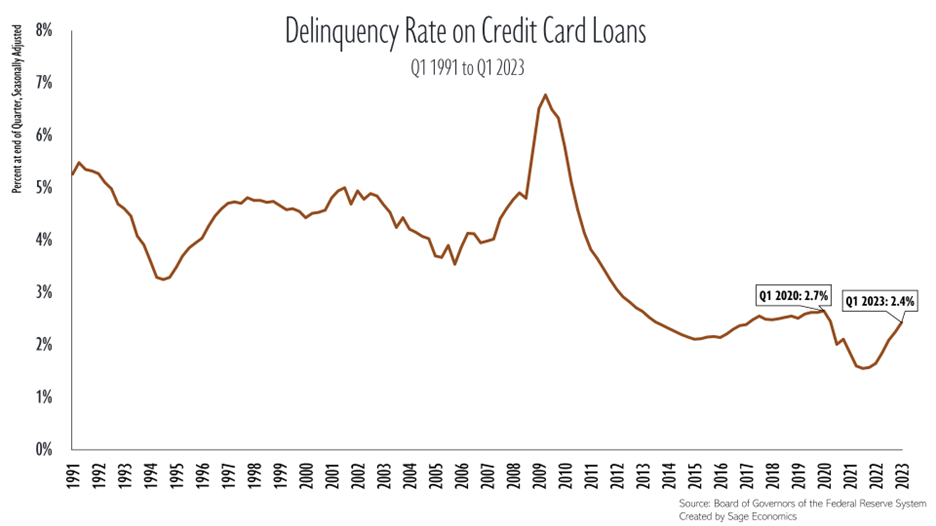

That’s according to some pretty encouraging data on delinquency rates that came out last Friday. While credit card delinquency rates rose for the sixth straight quarter, they remain below pre-pandemic levels.

So consumers’ financial health is worsening, but not at a rate that suggests imminent problems (back in February, we wrote a longer post about how well consumers were doing). Total credit card debt was also unchanged in the first quarter, according to this NY Fed data, another sign that consumers are weathering inflation.

And then there’s housing. The delinquency rate on residential loans actually decreased in Q1 2023 and is now at the lowest level since Q2 2006 (yes, the housing market was hurtling toward disaster in 2006, but the fundamentals are completely different right now. Less than 0.5% of the total mortgage balance held by commercial banks is 90+ days delinquent right now, roughly half the rate from Q2 2006, and the median credit score at origination for new mortgages is currently 52 points higher than it was back then).

So many homeowners are locked into low fixed rate mortgages that, barring a sizable increase in unemployment, mortgage delinquency rates should stay pretty low over the next couple quarters. For the broader economy, this is important. Mortgages currently accounts for about 71% of all household debt.

Businesses are also paying back their loans without issue. The delinquency rate on commercial and industrial loans fell to the lowest level since 2018 in the first quarter, while the delinquency rate on agricultural loans fell to the lowest level since the end of 2014.

Commercial real estate is a big concern at the moment, and there’s definitely pain coming for an office segment that has been quite literally hollowed out by the rise of remote work.

That pain has yet to show up in the data, though. The delinquency rate for commercial real estate loans rose to 0.76% in the first quarter, higher than 2019 levels but still below any data point recorded before 2017.

The Upshot

Even I—an optimist about the current economic situation—expect credit card delinquency rates to worsen over the next couple quarters. The personal savings rate has been inching higher since last summer but is still pretty low. That, along with inflation and the resumption of student loan payments in the next few months, will eventually catch up with consumers.

But for now, real consumer spending and real personal income keep trending higher, the unemployment rate sits at the lowest level in over 50 years, and Americans are paying their bills on time. As Anirban wrote last week, don’t let the elevated chance of recession later this year blind you to the economy’s current strength.

Actually the whole first paragraph

what impact would a national $15 min wage have on CC delinquency rates 4 quarters from now?