Construction's Boom of all Booms

The megaprojects wind down

Construction Trend Tuesday—sometimes even on Thursdays!—covers one (hopefully) interesting industry trend in a quick, two-minute read. You can access the archive of CTT posts here.

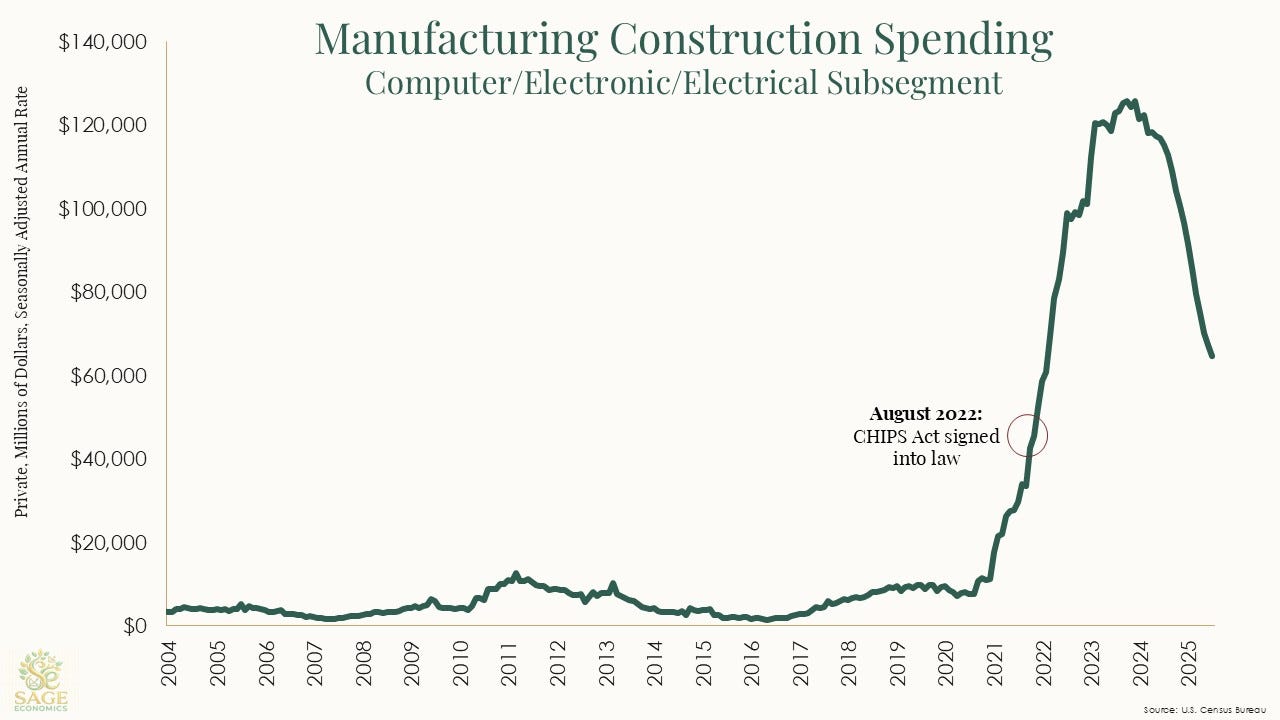

The computer/electronic/electrical manufacturing subsegment experienced the boom of all booms starting in mid-2021.

Spending in the category surged from less than $8 billion per year to a peak of about $126 billion in mid-2024, a stunning 1,500%+ increase.

The CHIPS Act deservedly gets a lot of credit for this, though it wasn’t signed until August 2022, about 12 months after the meteoric rise began.

Why did the boom start before the law was signed?

The semiconductor shortage spurred investment

The CHIPS Act didn’t just poof into existence in August 2022. Companies knew that it (or something like it) was in the works

Interest rates were historically low

This category also includes batteries, so other investments (like EVs) helped

This data series is nominal, and construction input prices took off in early 2021

Spending in this category has been falling—nearly as quickly as it rose—since late 2024. The construction intensive part of CHIPS Act megaprojects is winding down, EV supply chain investment has slowed, and interest rates have risen sharply.

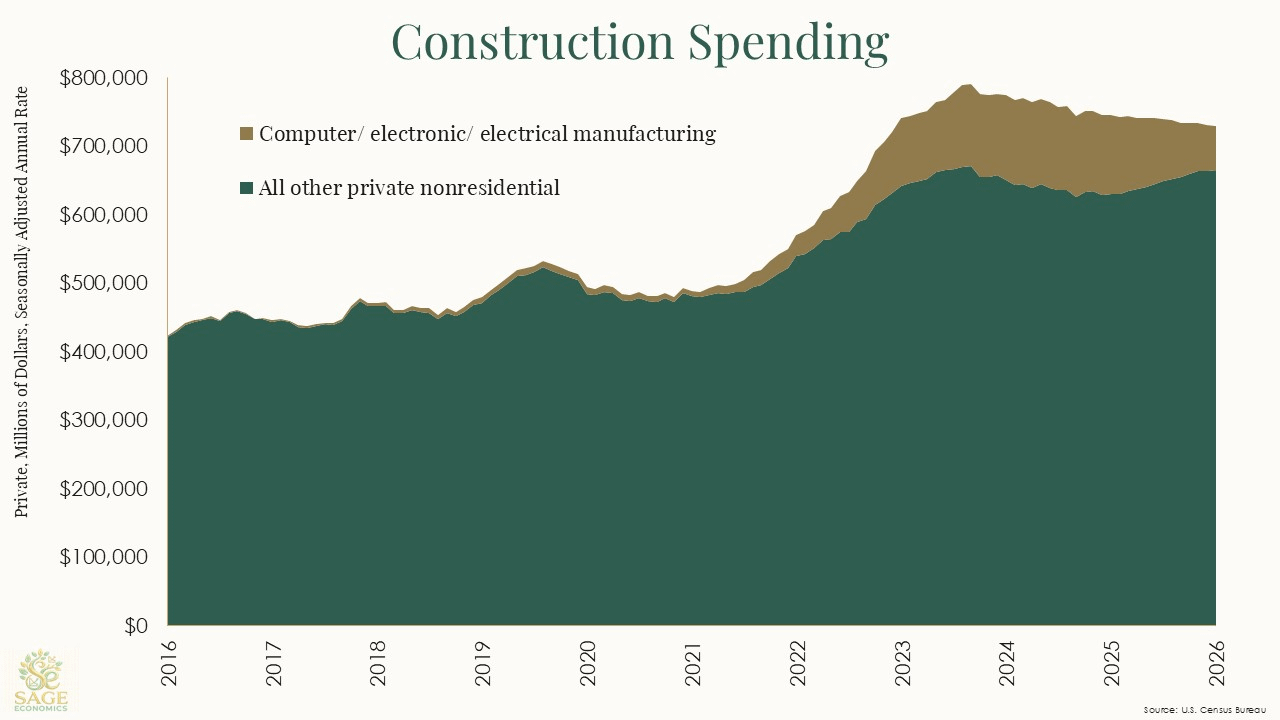

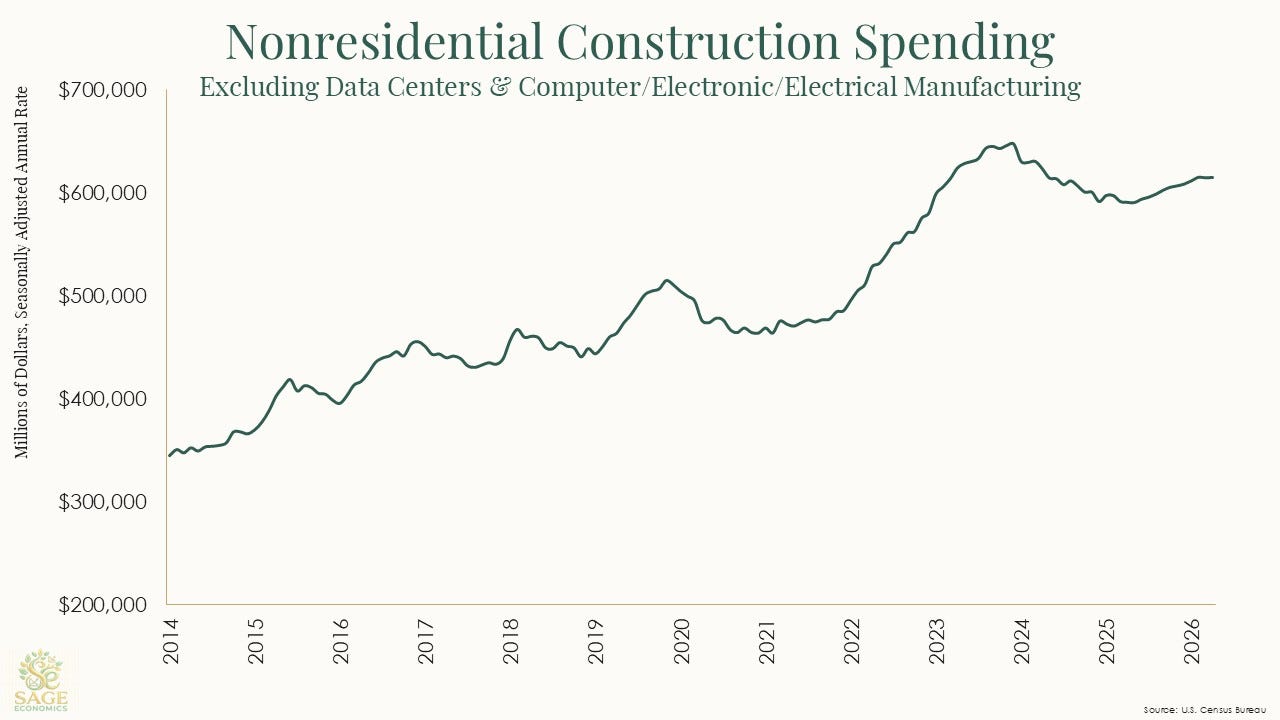

This rapid rise and fall has made it difficult to assess the broader nonresidential construction segment. Including that subsegment, private nonresidential spending has been in decline since late 2023.

Excluding that one subsegment, however, all other private nonresidential spending began to rebound at the start of 2025 and is less than 1% below the December 2023 all-time high.

And because we know you’re wondering: data centers account for 46% of the increase in all other nonresidential spending (the green part of the above graph) since January 2025. That’s a lot, but there’s still been modest growth across the remainder of the segment.

Big picture: the headwinds causing the computer/electronic/electrical manufacturing construction slowdown remain firmly in place, and the subsegment will continue to shrink over the next couple quarters. That will drag on total nonresidential spending, an important consideration when viewing the aggregate data.

What’s Next

Next up is Week in Review, our every-Friday post that covers all the economic news and data in a breezy, five-minute read.

Week in Review is only for paying subscribers. If that’s not you and you want it to be, just click the subscribe button.