Inflation, Retail Spending, & More

Week in Review: May 13-17

This week was packed with data releases, including updates on inflation, retail spending, new home construction, and a whole lot more. My takeaway is that the economy is slowing, inflation is trending lower, and the markets love it!

Monday

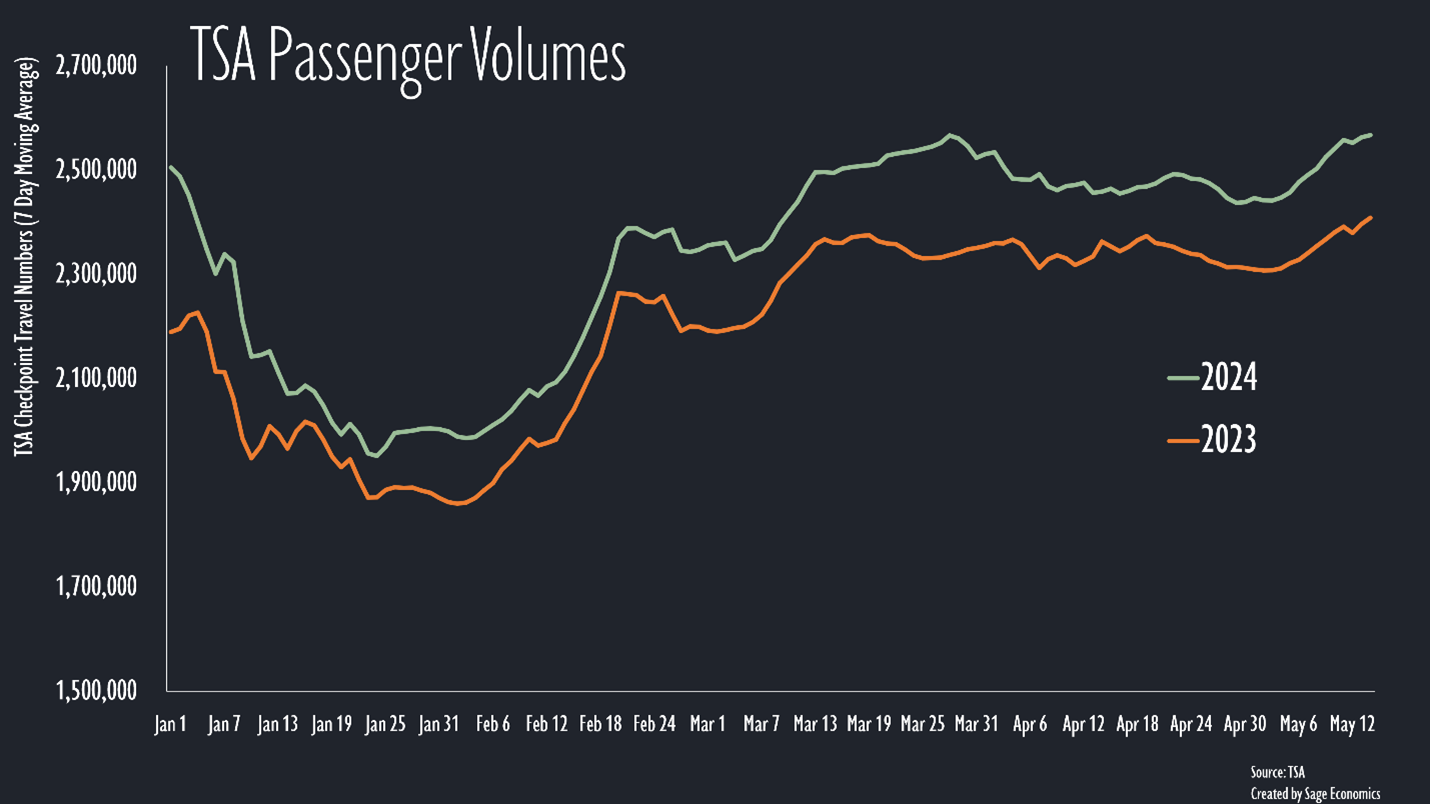

TSA Checkpoint Travel Numbers

The number of passengers screened by TSA remains well above 2023 levels. Whatever else is going on in the economy, people keep traveling, though I don’t know why so many people who look like triathletes pre-board.

Tuesday

NFIB Small Business Optimism Index

Small business owner optimism improved slightly in April, but owners remain pretty downbeat by historical standards due mostly to inflation. Wages have risen, insurance is more expensive, and a growing fraction of small businesses are being impacted by an emerging set of supply chain challenges.

Producer Price Index

This measure of inflation, which looks at prices received by U.S. producers, came in hot for April. Final demand prices (i.e., the last time something is sold) increased 0.5% for the month. If that happened every month, prices would increase more than 6% over the course of a year (not good!). Fortunately:

PPI is less important than CPI (see Wednesday).

This measure is up just 2.2% over the past year.

A large portion of the increase was due to higher gas prices and rising financial services fees, which rise with stock prices.

Gas Prices

Gas prices fell to an average of $3.73 per gallon and, because it looks like we’re past the spring peak, should continue to move lower over the next several weeks.

Diesel Prices

Diesel prices fell by about $0.04 per gallon last week and have now decreased in each of the past five weeks.