Labor Market Cooled in June

Could rate cuts come sooner than expected?

This post is sponsored by Pivot Workforce. I wouldn’t accept a sponsor for this newsletter unless they were: 1) a company I know and trust and 2) tackling an important problem like the construction industry's skilled labor shortages. Pivot checks both those boxes. Their goal is to help construction companies get the high-quality talent they need, and they have over three decades of experience staffing difficult-to-fill positions for some of the most recognized names in the construction industry. I urge any contractors struggling to find workers to give Pivot a look.

U.S. payroll employment increased by 206,000 in June. That’s a slightly larger increase than expected (+190,000) and a perfectly healthy rate of hiring. Viewed in pure isolation, the headline number is simply fabulous. But of course, as an economist, I can’t simply look at one number. I look at all of them, and that paints a more confusing, less refined picture. Ah, the Dismal Science!!!!

Here are some of the complications. April and May’s headline employment growth estimates were revised down by a collective 111,000 jobs. With those revisions, we’ve averaged about 177,300 jobs per month since April, the lowest three-month average since January 2021.

And then there’s the unemployment rate, which inched up to 4.1% in June, the highest rate since November 2021.

There is a silver lining here. The rising unemployment rate is largely due to more people looking for jobs. The labor force expanded by 277,000 in June, the fastest growth since March. Year-over-year earnings growth slowed to 3.9%. That’s the smallest annual increase since May 2021.

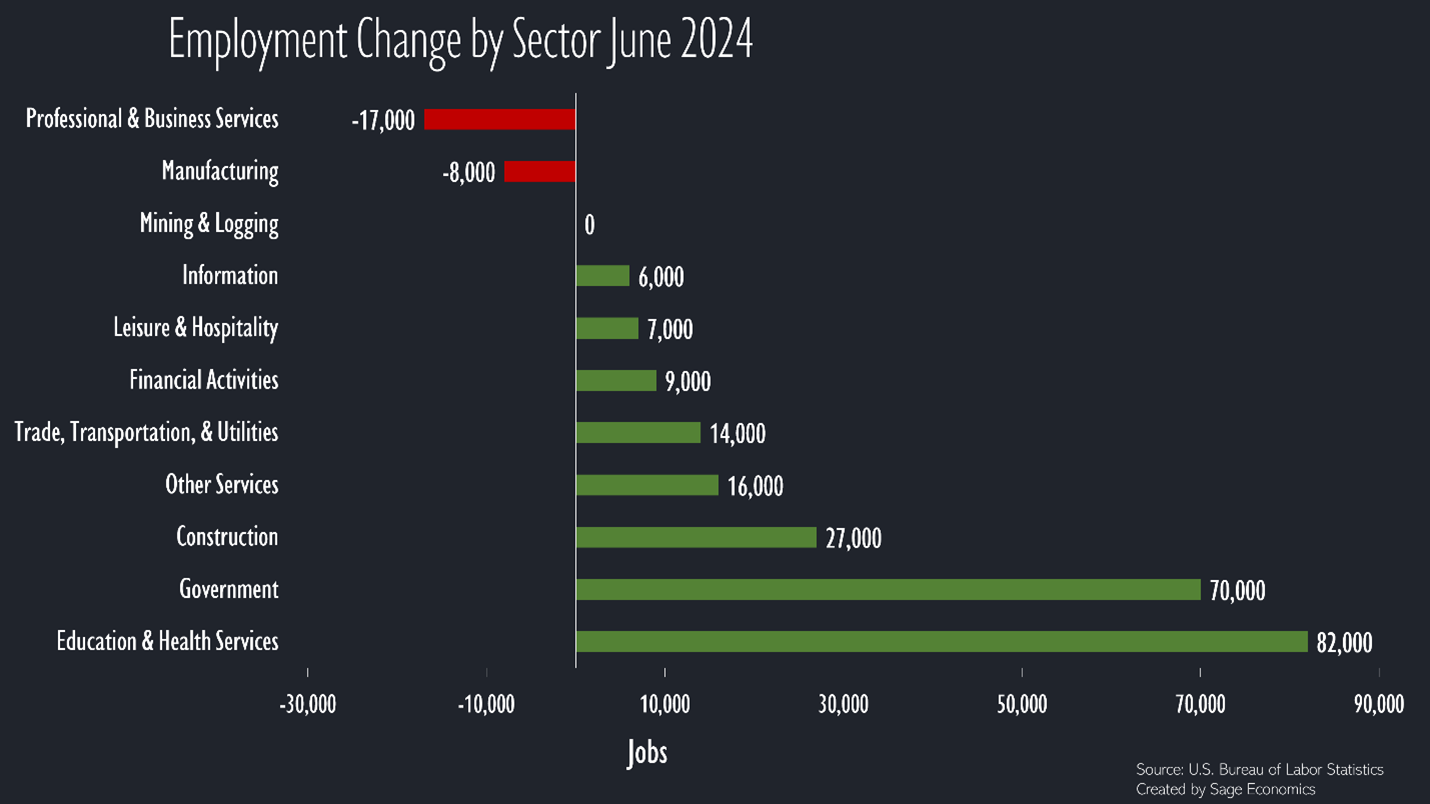

By sector

Job growth remains concentrated in the government and healthcare segments (they group private education and healthcare together, but private education actually lost 700 jobs for the month). On the government side, about half of the hiring occurred at the local, non-educational level. These are non-cyclical segments of the economy that aren’t especially interest rate sensitive. Because these jobs are non-cyclical, one cannot count on continued job growth from these sectors.

The construction industry also added jobs at a healthy clip in June, and you can read what I had to say about that over at ABC.

While it looks like professional business services suffered a brutal June, the monthly decline was entirely due to a 48,900 job decrease in temporary help services (think staffing firms).

On the one hand, some view this segment as a leading indicator of what hiring will look like a few months down the road (hesitant employers may begin hiring temporary staff before committing to permanent employees). On the other, this segment has been losing jobs since March 2022 and may simply naturally underperform when labor is scarce.

My view is that this is a canary in the coalmine and signals further slowing in the labor market going forward. That seems obvious, but the loss of temporary jobs at that magnitude indicates that the slowing in employment creation may be more rapid during the months ahead than what is presently built into consensus forecasts.

What do we take from this?

The Fed will like what they see in these data. The labor market is cooling, with job growth slowing and the unemployment rate gradually rising. None of this is inconsistent with a soft landing for the economy. That’s great, and the financial markets love it.

The notion is that the economy’s slowing remains gradual, limiting risk of recession. But with the economy slowing, the Federal Reserve may be positioned to cut rates once or twice this year (my guess, September and December of this year is when it begins) and then approximately four to six times next year. That will help shock the economy back to life, supporting faster economic growth, stronger corporate profit growth, etc.

The Fed will care more about next week’s CPI data than today’s jobs report, but viewed on its own, today’s jobs data suggest rate cuts could come sooner and more often than many anticipate.

What’s next?

We’ll have Week in Review, our every Friday post where we concisely cover everything you need to know about the economy, out in the next couple hours. That’s just for paying subscribers. If that’s not you and you want it to be, just click the button below:

Want to see me speak?

My 2024 presentation is Clint Eastwood themed. If you want me speak to your organization (either virtually or in person), just reach out to my assistant Julia at Jcomer@sagepolicy.com.