March 2023 Jobs Report

Job growth slowed, and that's just fine

This post is sponsored by Pivot Workforce. I wouldn’t accept a sponsor for this newsletter unless they were 1) a company I know and trust and 2) tackling an important problem like the construction industry's skilled labor shortages. Pivot checks both those boxes. Their goal is to help construction companies get the high-quality talent they need, and they have over three decades of experience staffing difficult-to-fill positions for some of the most recognized names in the construction industry. I urge any contractors struggling to find workers to give Pivot a look.

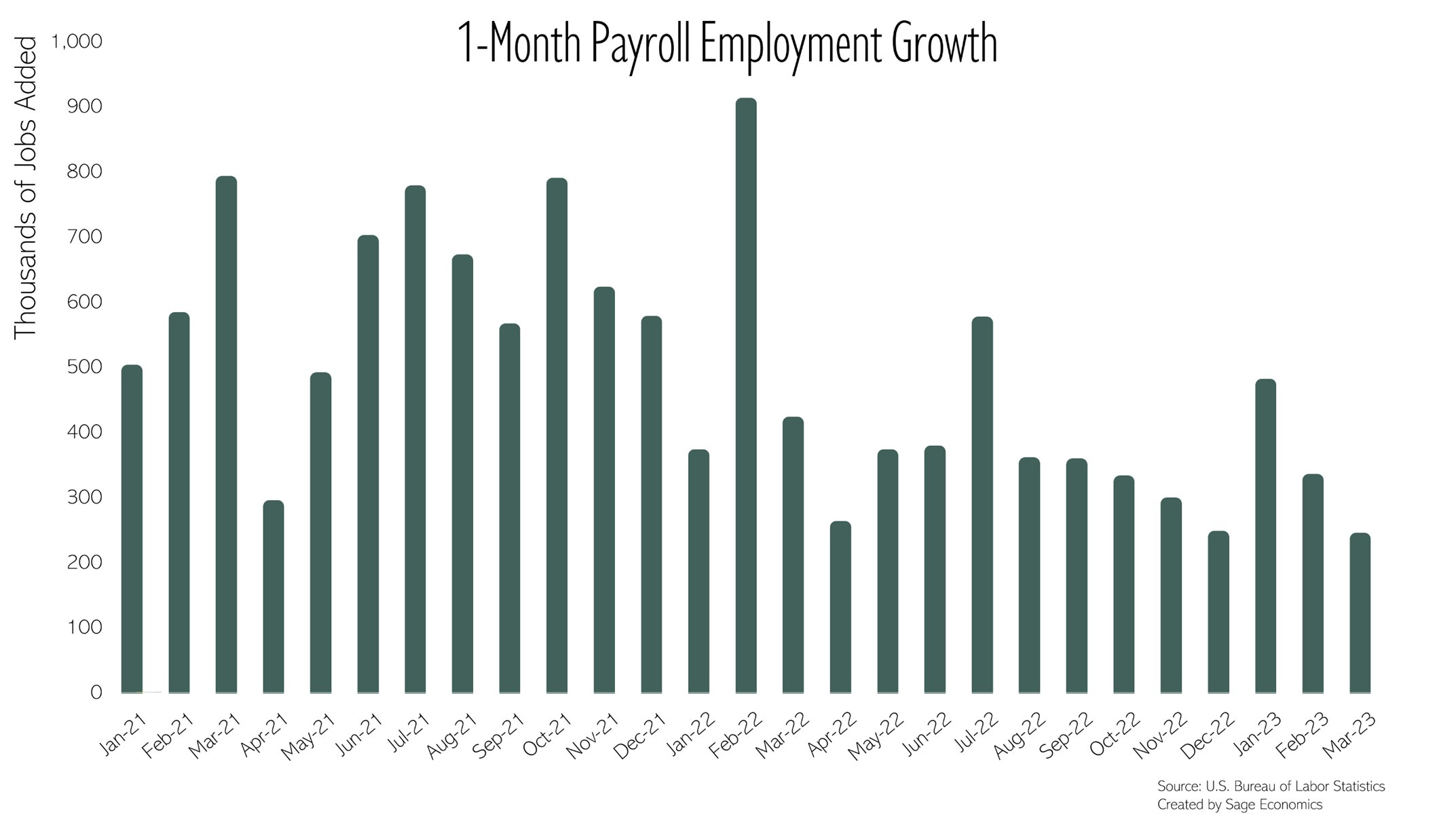

U.S. payroll employment increased by 236,000 in March, which is about exactly what was expected. After eleven straight months of job gains coming in stronger than expected, it’s nice to see forecasters finally get one right. This is the slowest month of job growth since December 2020 but still well above pre-pandemic levels.

The unemployment rate slipped back down to 3.5%. That’s way too low, but it’s not all bad news on the labor availability front. The labor force expanded by 480,000, and the labor force participation rate inched up to 62.6%. That’s the highest LFPR since March 2020 but still 0.7 percentage points below the February 2020 level.

Wage growth accelerated just slightly on a monthly basis (+$0.09, 0.27%), but that monthly pace translates to a perfectly acceptable 3.4% annualized rate. Actual wage growth from March 2022 to March 2023 came in at 4.2%, which is the slowest pace since the third quarter of 2021.

So job gains look to be slowing but are still strong, the LFPR keeps ticking higher though the labor supply remains historically tight, and wage pressures appear to be moderating. This is pretty ideal considering what we could reasonably expect from today’s report; we want to see growth cool, but we want it to cool slowly.

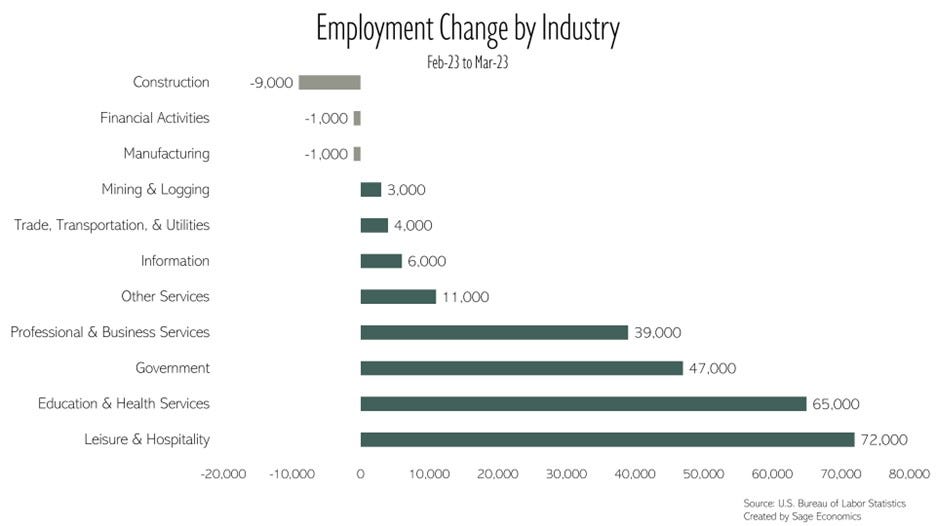

Job gains were concentrated in sectors that had been struggling to attract workers: leisure and hospitality (+72,000), health care and social assistance (+50,800), and government (+47,000). Leisure and hospitality is still 368,000 jobs (2.2%) away from returning to February 2020 employment levels.

A few sectors lost jobs in March. Construction payroll employment fell by 9,000 (read what Anirban had to say about that over at Associated Builders and Contractors). Retail trade (a component of trade, transportation, and utilities) lost 14,600 jobs, but that’s also due to the construction industry—about 58% of those lost retail jobs (8,500) were at building supply and garden equipment and supplies dealers.

The manufacturing industry lost 1,000 jobs for the month, adding to a slew of weak manufacturing data over the past week. We’ll cover that at length in our Week in Review post later today. That’s just for paying subscribers. If you want that to be you, just click the button below:

Three (somewhat) Key Takeaways

The prime age (25-54) employment-population ratio (80.7%) is now at its highest rate since 2001. This is a tough one to swallow for the “nobody wants to work anymore” crowd.

Those with at least a bachelor’s degree accounted for almost all of the labor force growth in March.

The public sector has yet to recover all the jobs lost in early 2020, with employment still 314,000 (1.4%) short of February 2020 levels.

What to Watch

It’s still all about inflation, and we get new Consumer Price Index and Producer Price Index data next week.

Want to Hear Anirban Speak Live?

His 2023 presentation is called Show Me the Money (Supply), and yes, the theme is Tom Cruise movies. If you want to book a presentation (in person or virtual), please contact his assistant Julia (jcomer@sagepolicy.com).