Week in Review: March 14-18

A third week of assault on democracy in eastern Europe continued to wreak havoc on oil price stability, and rising COVID-19 case counts in Asia and Europe added fuel to the fire. Global supply chains will remain in disarray as a result, and that’s no surprise.

But here is a surprise: during another week of Putin, pandemic, and price instability, oil prices actually declined for much of the week. They surged to a high of $123.70 on March 8 before dipping back below $100 about a week later. As of this writing (Friday morning), oil is still sitting at a lofty $104/barrel, but that’s far less than what many pundits had forecast.

In response, financial markets, which are off to their worst start since 1957 when the Baltimore Colts went 7-5 in the NFL West division, rallied. Investors appear to be awaiting word of a ceasefire and eventually a resolution involving a departure of Russians from Ukraine. And yes, that could turn out to be naïve.

There wasn’t any economic data released on Monday, so let’s go right to . . .

Tuesday

Daylight Saving Time

The Senate passed the Sunshine Protection Act, a measure that would make Daylight Saving Time permanent, by unanimous consent. It still has to pass the House, but this seems like a popular move. If you’re wondering who’s opposed, the National Association of Convenience Stores successfully lobbied to extend the clock changes in 2005 citing the positive effects on commerce (coffee and cigarette sales as people strive to stay upright?), and this group is at it again (menthols please with cream and sugar). The proponents’ other argument is that moving the clocks back and forth conserves energy, which seems to be at odds with reality.

Producer Price Index (PPI)

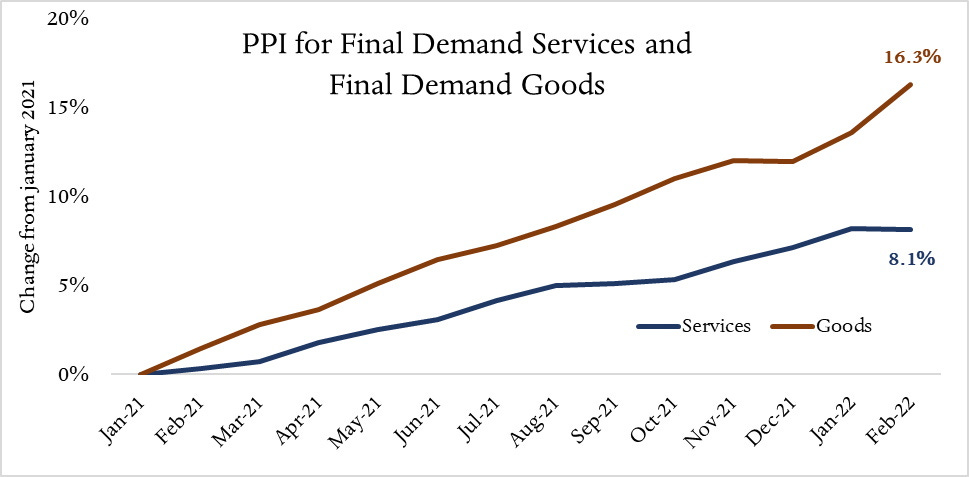

PPI measures the average change over time in the selling prices received by domestic producers, and the reading for final demand goods jumped 0.8% higher in February, less than forecasters expected but still more than is generally acceptable to your average American. True, this was the best inflation-related news in a while, but that just reminds us how problematic inflation has become. Final demand prices are up 10% since February 2021.

The pandemic caused spending on goods to soar in both absolute terms and relative to spending on services (think all those people who bought furniture instead of a taking a vacation), and that’s one of the driving forces behind inflation as the global supply chain has buckled under the literal weight of all these goods. That dynamic remained apparent in February’s PPI data. Final demand goods prices rose 2.4% for the month while final demand services prices were unchanged. Since 2021’s onset, final demand goods prices are up 16.3%, more than twice the 8.1% increase in prices for final demand services.

You can read my thoughts on construction input prices over at Associated Builders and Contractors.

The IRi Supply Index ™

The IRi Supply Index™ indicates that 87% of edible products and 92% of nonedible products were in stock for the week ending 3/13/22, virtually unchanged from the same week in February. I’m rooting for edible products, and have them taking out Arkansas and Gonzaga in the West regional.

Wednesday

Retail Sales

Retail sales climbed 0.3% in February. Not only is that less than the 0.4% increase expected by forecasters, its slower than the rate of inflation, meaning that retail sales fell in real terms. Total retail sales excluding gasoline stations actually declined 0.2% in February, and these data predate the surge in gas prices.

This probably sounds pretty dire, but it shouldn’t. Retail sales absolutely sky-rocketed in January (+4.9% for the month, +14% year over year) and sales rose significantly faster than inflation over 2022’s initial two months. The nation has added about 565,000 jobs a month since the start of 2021 (often at high wages, which is inflationary but also drives purchases) and consumer demand will remain strong as long as that trend persists (historically elevated job openings suggest it will).