November Jobs Report a Cause for Concern

Wage Increases Accelerate

This post is sponsored by Pivot Workforce. I wouldn’t accept a sponsor for this newsletter unless they were 1) a company I know and trust and 2) tackling an important problem like the construction industry's skilled labor shortages. Pivot checks both those boxes. Their goal is to help construction companies get the high-quality talent they need, and they have over three decades of experience staffing difficult-to-fill positions for some of the most recognized names in the construction industry. I urge any contractors struggling to find workers to give Pivot a look.

America's employers collectively added 263,000 net new jobs in November, the fewest since April 2021.1 But that figure was meaningfully above the consensus estimate of 200,000 jobs added. The unemployment rate stayed pinned at 3.7%. In short, the labor market is still hot.

Many will celebrate a still strong employment market, including jobseekers, parents of graduating students, underperforming workers, and certain politicians. But make no mistake, there is plenty of cause for concern.

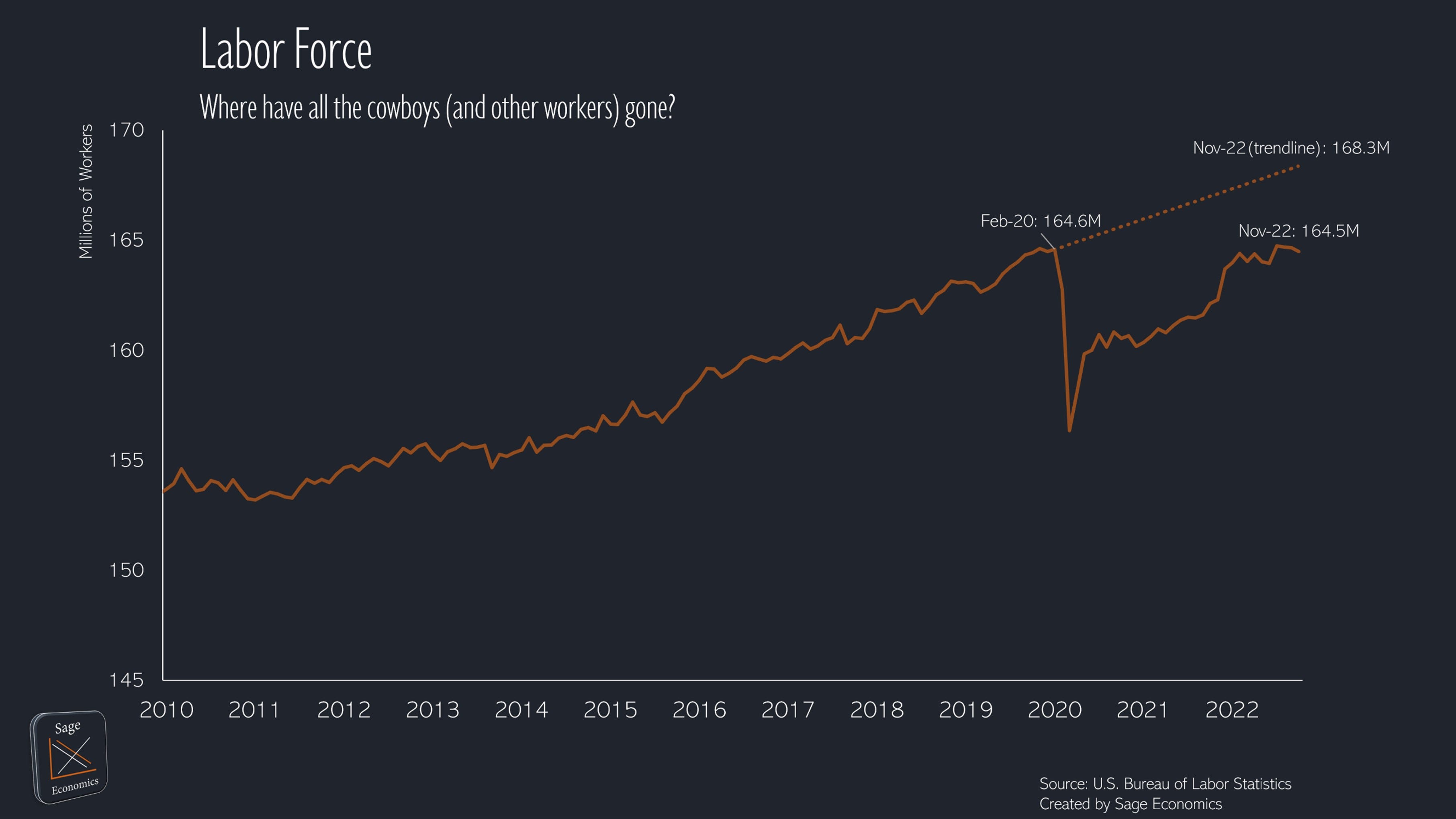

Here’s what Zack the Millennial has to say about it: “The labor force shrank for the fourth time in five months in November, down another 186,000 people. There are now about 265,000 fewer people either working or looking for work than in August and just 72,000 more than in March. Put simply, that’s bad.”

That’s right, Zack, that’s bad. And I have to admit, I’m (Anirban Basu, GenXer known as Economist X to myself and none other) surprised that more people are not jumping back into the labor force. After all, people are increasingly struggling to pay their bills amid rampant inflation. Just how large were those stimulus payments?

Because the economy remains overheated, businesses are still hiring aggressively. But there aren’t nearly enough people to fill available jobs, and that pushes wages higher. Average hourly wages increased $0.18 in November, more than twice the consensus forecast. As if that weren’t enough, there was also a significant upward revision to October’s wage growth.

Now you may consider me a curmudgeon. Shouldn’t I be happy that people are making more money? Well, I would be happy if it weren’t negatively impacting me. All this inflation is deeply upsetting, and then there’s the Fed . . .

That’s the real story here. The Federal Reserve will need to put the brakes on the economy harder and longer (sounds like a Prince song I used to like) to restore inflation to its 2% target. Our central bank has been raising interest rates since March, but there’s more to come. Even if the Fed sees fit to stop raising rates early next year, they will have to keep them elevated to sufficiently dampen economic momentum and get inflation down. To date, the labor market is not cooperating.

While some economists (lesser beings) will claim that today’s strong employment report renders recession less likely, they’re absolutely wrong. This makes it more likely that a downturn is coming to America over the next 12 months as interest rates stay high and the yield curve remains inverted.

There was a ton of other economic data—the most in any week since we started doing this newsletter—that we’ll cover in the Week in Review post later today. That’s only for paid subscribers, so if you’re interested, click the button below:

As always, you can read Anirban’s in-depth thoughts regarding the construction industry’s labor market at Associated Builders and Contractors.

Three (somewhat) Key Takeaways

The retail sector lost 29,900 jobs in November. The transportation and warehousing sector lost 15,100. It looks like demand is starting to crack, and that’s impacting both brick and mortar retail establishments and e-commerce.

The temporary help services segment lost 17,200 jobs in November. That’s usually considered a sign that hiring is about to weaken, but I think the labor market may be so tight that job seekers are simply bypassing temp help agencies.

Average weekly hours fell to 34.4, putting it back to where it was in February 2020. Average weekly overtime hours for manufacturing employees is now below February 2020 levels.

What to Watch

Inflation, obviously, but I’ll be interested in November retail sales data. There are indications that consumers are beginning to pull back, but it hasn’t showed up in much of the spending data yet.

Want to Hear Me Speak Live?

Of course you do. My 2023 presentation is called Show Me the Money (Supply), and the theme is Tom Cruise movies. If you want to book a presentation (in person or virtual), please contact my assistant Julia (jcomer@sagepolicy.com).

The initial estimate of October’s job gains was lower than this at +261,000, but that was revised upward to +284,000. September’s estimate was revised down from +315,000 to +269,000, so net job growth for September and October was revised down by 46,000 in today’s report.

Not sure I understand or maybe I missed you reporting on this. Do we know the net gains losses from baby boomer retirees vs GenZ or whomever is the current generation to enter the work place