Inflation: What (and Who) to Blame

Let’s look at an oversimplified model. Assume the supply of and demand for widgets was 10 before the pandemic. Covid comes, lots of people lose their jobs, ports close, people stay home to be caretakers, materials are hard to find, etc.

Now consumers only want to buy 8 widgets and suppliers can only manufacture 8 widgets. The government, trying to avoid an economic cataclysm, sends out stimulus checks. These checks bring the demand for widgets back to 10, but the supply of widgets remains at 8.

Prices might not rise immediately, but two would-be widget buyers are now left widgetless. Some who do have widgets start selling them secondhand for more than MSRP. Producers try to expand operations to make more widgets, but now they have to pay more for widget inputs. The workers at the widget factory also buy widgets, and now that widgets cost more (along with anything else mired in these dynamics) they demand higher wages.

Mechanisms aside (and this isn’t nearly all of them), the important thing is that the price of widgets went up. Who’s to blame?

The widget supply chain (i.e. supply)

Widget buyers (i.e. demand)

The “greedy” corporations that make and sell widgets

The “ungrateful” workers at the widget factory

The “president” who sent out the stimulus checks (or at least took credit for it)

Covid-19

All of the above

If it makes it easier, assume the president is from the other party. But blame game aside, there’s no single, simple answer.

Shifting Demand Dynamics

At the start of the pandemic, a lot of people lost the ability to spend on services (think restaurants, concerts, vacations, etc.) because they were essentially confined to their homes, which they realized were in need of some updating. So people couldn’t spend on services, got stimulus checks from the government, and were in many cases flush with cash (and time at home with their computer and Amazon.com). Spending on services plummeted, spending on nondurable goods rose, and spending on durable goods absolutely surged.

Nondurable Durable goods1 are things that don’t wear out like cars, appliances, and bicycles, but let’s just call them widgets for consistency’s sake. The demand for widgets went way over 10, the supply of widgets was way below ten (these larger widgets are difficult to ship, especially during a global pandemic), and prices went up.

The notion that inflation was transitory was partly based on the assumption that the relative demand for goods and services would normalize once the pandemic ended, but the pandemic stubbornly refused to end, and as you can see in the chart above, demand for goods is still well above the pre-pandemic trend while the demand for services is still below it.

There are signs that these dynamics are reverting to some semblance of normal, but it’s been slower than anticipated. I suspect that surging energy prices (thanks, Putin) have put a serious dent in what would have been a big rebound in travel this summer (airline fares are up 37.8% over the past year). Another issue is widespread labor shortages that have made certain services (like dining out) less enjoyable than it used to be. Speaking of…

Labor Supply: No One Wants to Work Anymore

This is, obviously, an economywide issue, but let’s start smaller with the restaurant industry. As of May 2022, U.S. restaurants and bars employed about 750,000 fewer people than they did in February 2020, and restaurant employment was still 6.4% below pre-pandemic levels, while economywide employment was down just 0.5%. At May’s rate of hiring (a healthy 46,000 net new jobs), the restaurant industry won’t return to February 2020 employment levels until the end of 2023.

Restaurants have a few options on how to respond. First, they can pony up and pay higher wages to staff up. Assuming they do this, they can either cut their profit margins (the restaurant biz is notoriously low margin) or pass those higher wage costs on to consumers. They could also have fewer employees, the same number of tables, and slower service.

Of course, these strategies aren’t mutually exclusive, and data and personal experience suggest they’ve gone with all three. Average hourly wages for restaurant employees are up 16.8% since the start of the pandemic, well above the 11.5% increase seen across all industries. Importantly, overall inflation is 12.5% since February 2020, higher than the wage increase across industries but well below the increase in restaurant wages.

Anyone who’s been going to restaurants lately can tell you that A) they’re largely short staffed and B) service has suffered (anyone with a heart won’t be a jerk about it while they’re at the restaurant).

So that gives you a sense of how labor shortages push prices higher, which leaves us with two questions. Are labor shortages to blame for inflation? And are there labor shortages because nobody wants to work anymore?

The first question comes down to a simple truth: wages go up, prices go up. If you run a business and have to pay more for workers, you’re going to charge more for whatever it is you sell (let’s ignore the concept of a wage-price spiral since the relationship between price and wage increases is significantly more complex but nonetheless real). So to the extent that labor shortages have pushed wages higher, yes, a lack of available workers has contributed to inflation.

But why do we have these labor shortages? Again, several answers here, and fortunately I just answered this question in the most recent Q&A post. I’ve paraphrased the same answer below (if you already read that, skip to Was There Too Much Stimulus):

If I had to pick one reason? Retirement. So yes, a lot of people just don't want to work, and the American Dream has become early retirement. Here’s more from Zack:

While it might be true that people don’t want to work (I certainly don’t), the data show that they are. The prime age (25-54) employment to population ratio rose to 79.9% in March, about half a percentage point below February 2020 levels but higher than at any point from 2008 to July 2019, while the prime age labor force participation rate is back at 2019 levels.

So why are there so few workers? In classic millennial fashion, I’m going to blame this on just about every generation but my own. Let’s start with Baby Boomers. The employment-to-population ratio for 55+ is at 37.7%, well below the prevailing level of the past decade. We can mostly chalk this one up to retirements (I don’t think Boomers are smoking pot and playing video games in their parents’ basements, or at least not in large numbers).

We can also heap a little blame on Gen Z, albeit less than I’d like. The labor force participation rate for the 20-24 age range is modestly below 2018-2019 levels but above 2014-2017 levels, so they’re participating in the labor market at a decent rate.

Even in the aggregate, the employment-to-population ratio is above 2009-2016 levels and right on par with 2017. The worker shortages are (if you ask me) a function of low immigration rates (due to both pandemic and policy, though more ideas like this would help), the long-term decline in fertility rates, and covid-induced early retirements. The notion that people don’t want to work anymore is a convenient and popular explanation, but one that I don’t really buy.

Was there too much stimulus?

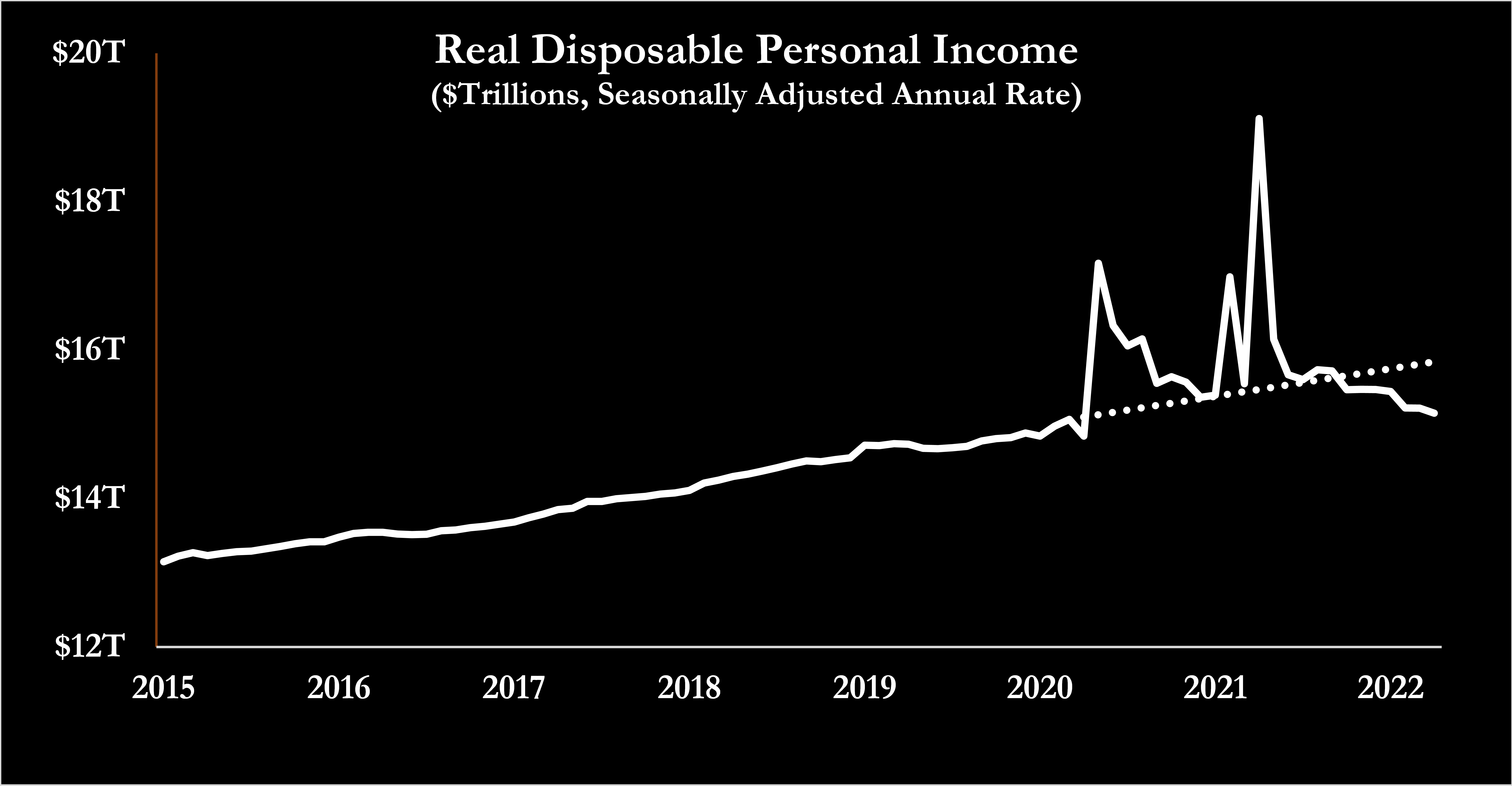

Yes, but that’s easy to conclude and state in hindsight. At the time of the relief packages, the notion that it was better to miss high than low was pretty widespread. Whether or not that’s true, the influx of stimulus-infused personal income definitely contributed to inflation.

Look at the chart below. Can you tell when the three relief packages hit the economy (two signed by Trump, one by Biden)? If you guessed May 2020, February 2021, and April 2021, congratulations, you know how to read a line graph. If you scroll back up to the first graph of spending, you can see the coinciding increases in spending that occurred shortly thereafter.

Now think back to our widget scenario. Those infusions of personal income pushed the demand for widgets back to ten (or to eleven if we want to invoke the majesty of Spinal Tap), while supply of widgets and materials and labor needed to make widgets remained constrained.

It’s impossible to know what happens under a counterfactual in which we issue significantly less stimulus. Obviously, there’s a Goldilocks level that would have cushioned the harmful economic effects of the pandemic while causing relatively less inflation, but the more concerning issue is what would have happened if we undershot that. Unfortunately, I don’t have a firm answer to that, and it’s hard to balance the tradeoff between people’s jobs/businesses still existing and a prolonged period of elevated inflation.

Can we still blame politicians?

Yes, please do and always. Beyond stimulus payments, Trump implemented tariffs on about 17% of U.S. imports, and tariffs are inflationary. Then Biden kept those tariffs in place. Trump paused student loan repayments, and Biden has yet to reinstate them because that would obviously be political suicide on his side of the aisle.

These are just a few of the many, many examples, but that three-month gas tax holiday that’s getting thrown around at the moment? Yep, that would be inflationary too.

How much should we blame Putin?

A lot. Inflation would be far milder without the resulting surge in energy prices, and the Fed almost certainly wouldn’t have needed to implement the first 75 basis point rate hike since 1994 earlier this month. Underlying inflation (i.e., the inflation the Fed has the ability to affect) is probably around 4%, depending on the estimate, well below the 8.6% that shows up in the headline number. Because this one is pretty straightforward and also out of our policymakers’ control (relatively speaking), I don’t think much more needs to be said on it.

Conclusion

This is a boring answer, but there’s no one culprit here. Beyond the confluence of factors mentioned above, inflation causes more inflation (when inflation is less widespread, inflation can also cure inflation). There’s no silver bullet to bring inflation down, and really, the Fed is pretty limited in what kind of bullets it can use. Interest rates are rising, and a soft landing looks increasingly unlikely. Widget prices will come down eventually, but two big questions remain: when, and how much economic hardship will be caused in the process? Perhaps we can discuss risk of recession next time around.

Looking Ahead

Week in Review on Friday will feature home sale data, a few composite indices, and more. If you’re not a paid subscriber and want more than a free preview, click the button below.

This originally had a typo that said “Nondurable goods” when we meant “durable goods.” We obviously regret the error, but also hope you knew what we meant.

So Anirban/Zack-- in regards to restaurants being short staffed-- you didn't mention immigration. I know some restaurants for dishwashers, grunt workers-- definitely were a little laxed in checking for legal status. And they also used legal immigrants of course. Question-- what if we made it easier for hardworking, law abiding, GRATEFUL immigrants to come to the US. How would this affect the service industry labor shortage and how would it affect inflation. Easier question ;)-- why can't congress figure out how to let more legal immigrants in?

While Putin deserves some blame for pushing energy prices up further, energy prices were already rising in the last half of 2021 as the post-pandemic economic recovery outstripped several years of underinvestment in oil and production (which resulted from an extended period of low energy prices), the concurrent dispersal of energy workers (including pandemic reductions), and political policy limiting fossil fuel supply (Keystone and federal leases, etc.).